The Aapryl Quarterly Market Insight offers a lens on how active managers in general performed in various markets and sub-segments. Using Aapryl’s proprietary methodology, we measure manager skill by using the manager’s static clone (long term factor profile) as a measure of skill instead of the broad market benchmark. Manager skill is calculated by using the manager’s raw return less their static clone return.

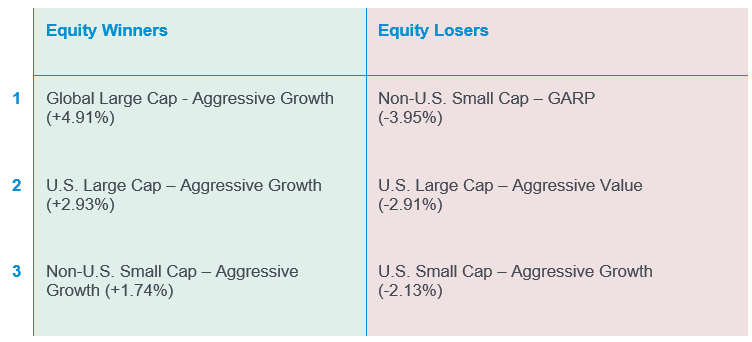

The 2nd quarter of 2025 reversed the performance dominance of Value, while Growth took centerstage for median managers. Global Large Cap Aggressive Growth was the best peer median group +4.91%, which extended down to U.S. Large Cap Aggressive Growth +2.93% and Non-U.S. Small Cap Aggressive Growth +1.74%. The worst performing peer median was Non-U.S. small Cap GARP -3.95% followed by U.S. Large Cap Aggressive Value -2.91% and U.S. Small Cap Aggressive Growth -2.13%.

Below are the top three winners and bottom three losers based on the performance of their respective peer group medians for the prior quarter:

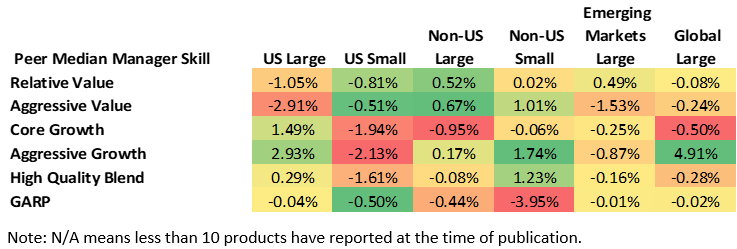

Aapryl Peer Group Manager Skill Performance Matrix

Quarter Ending 6/30/2025

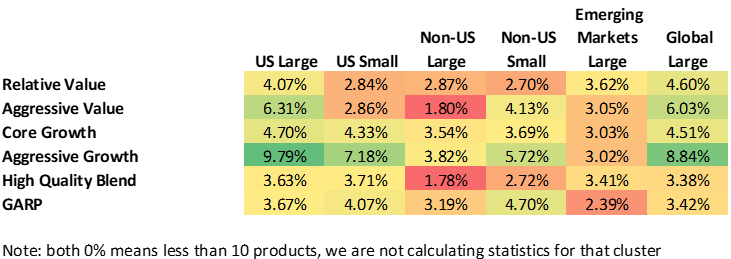

The performance spread between the top and the bottom quartile within their respective peer groups varied for each Aapryl peer group is shown below. This quarter we saw a big spread differences in almost all of the peer groups. The biggest performance spread between the peer groups top quartile vs bottom quartile reversed from U.S. Large Cap Aggressive Value peer group to U.S. Large Aggressive Growth +9.79% this quarter, with the lowest spread occurred in U.S. Large Cap Aggressive Value +1.80%.

Top Quartile vs. Bottom Quartile

Quarter Ending 6/30/2025

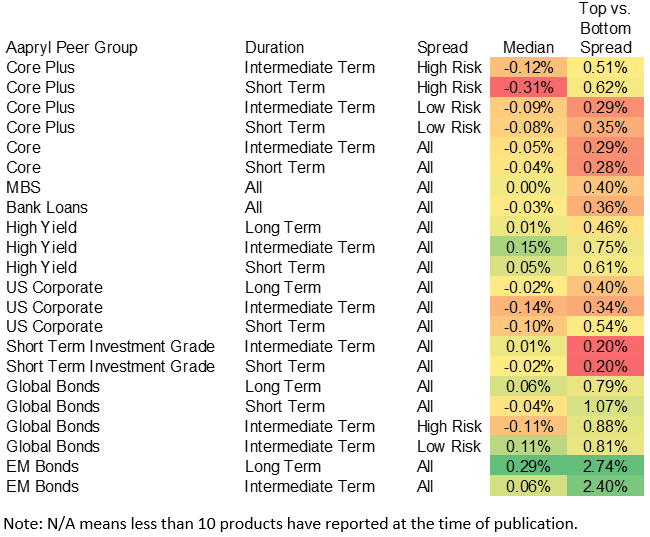

Fixed Income Manager Performance During the Quarter

Active managers in Fixed Income continue to show performance differences between top and bottom quartile managers. The highest spread this quarter continued to be in EM Bond Long Term All Spread +2.74%, while Short Investment Grade Intermediate Term and Short Term All Spread both had the lowest spread of +0.20%. The EM Bond Long Term All Spread median managers performed the best with +0.29%, while Core Plus Short Term Spread High Risk performed the worst during the quarter with -0.31% median return.

Quarter Ending 6/30/2025